One thing I noticed during my 34 years (1986 to 2020) practicing law in Oregon, if you knew how to play the game, non-disabled people could “qualify” for monthly Social Security Disability benefits which, if one timed it right, would guarantee lifelong monthly payments more than the person would receive as a retiree.

STEP ONE: TRANSFER $$$ FROM DISABILITY FUND TO RETIREMENT FUND

The Social Security Retirement trust fund faces an imminent funding shortfall, according to the latest annual report from the program’s trustees, released on June 9th. The Old-Age & Survivors Insurance (OASI) Trust Fund reserves are projected to become depleted in the fourth quarter of 2032, with 78 percent of benefits payable at that time, thus cheating American retirees who paid into the system for 40-50 years.^ [This translates into about a $500 monthly reduction for the average retiree.] The Disability Income (DI) Trust Fund reserves are projected to remain positive throughout the 75-year projection period.

Absent action from Congress, the trust fund used to pay benefits to retired workers, their spouses, minor children and survivors of deceased workers, may run out in the fourth quarter of 2032, according to the report, several months earlier than had been projected last year.

If no changes are enacted by 2032, lawmakers may opt to extend the program’s funding slightly by combining the retirement and disability trust funds. Social Security’s trustees estimate that this would bring the depletion date to the third quarter of 2034, when 83% of scheduled benefits would be payable.

STEP TWO: CHANGE QUALIFICATIONS FOR DISABILITY PAYMENTS

In the 2026 Annual Report to Congress, the Trustees announced: The reserves of the combined OASI and DI Trust Funds declined by $160 billion in 2025 to $2.56 trillion. The annual cost of both the retirement and disability programs are projected to exceed annual income in 2026 and remain higher throughout the 75-year projection period. Total cost began to be higher than total income in 2021. Social Security’s cost has exceeded its non-interest income since 2010. Yet, the US House and US Senate could not be bothered to study the issue and fix it. The Senate-confirmed Commissioner of Social Security has the authority to make the following changes:

First, major changes must be made to reduce the number of new disability recipients by significantly tightening the types of “problems” which deem a person unable to earn a living. To do so would not require Congressional approval. Suggestion: The “problem” must be a new disability due to a recent illness or recent accident. I had a client in her 40s, who had been gainfully employed most of her adult life UNTIL she was awarded disability benefits because she had a “low IQ.” When mentally retarded people (IQs under 70) are gainfully employed, why should a lazy person receive SS DI?

Second, most current recipients of disability income should be re-evaluated under the new, tightened rules, starting with those whose “disability” cannot be discerned by the average stranger who meets the recipient in a store or on the street or at a social event. I had a very tall client, in his late 20s, who was a star on Portland’s intramural city basketball team. He was receiving SS DI payments.

Third, when a person reaches a certain age, he cannot get disability payments for having knee replacement surgery. One of the schemes I learned from my clients: Clients in their late 50s or early 60s, they timed their knee replacement surgery just before they planned to retire. Why? Because Social Security Disability payments are higher than Social Security Retirement payments. This was VERY COMMON and VERY WELL KNOWN among blue-collar workers. Surely, Social Security administrators are aware of this scheme, too. Alternatively, SS administrators could give these workers with new knees the same about of “disability” payments as they would get in retirement payments.

Fourth, a federal retiree’s retirement benefit is 40% of his/her three highest years of federal income. Social Security Disability Income should be calculated the same way.

Fifth, if the person is eligible for permanent Workers Compensation benefits and/or permanent VA disability benefits and/or any other type of taxpayer-funded disability benefits, he/she should not be eligible for Social Security Disability benefits or, the SS DI benefits should be lowered due to receipt of the other monthly payments. I have had a number of clients over the years who were receiving, altogether, double or triple what they they were making when employed. Taxpayers should not be on the hook for this largesse.

Sixth, audits should be performed a year or two after every recipients’ payments begin, whether retirement, spousal, disability or survivor. Perhaps random audits are already being performed; but, I had a number of widows, who had never worked outside their homes who were receiving spousal benefits that were way too high. A spousal benefit is supposed to be 50% of the worker’s benefit. The following case sticks in my memory:

About 15 years ago I had a client who was receiving $2500 per month in Social Security benefits. When I inquired what type of work she had done she told me she had never worked. Since my father-in-law, who was about her age, was receiving only $2900 AND HE HAD ALWAYS PAID THE MAXIMUM IN SOCIAL SECURITY TAXES HIS ENTIRE WORKING LIFE, I knew that someone at the Social Security office had made a big mistake and that they had never audited her file. She had been receiving $2500 per month for about 25 years. The average monthly Social Security spousal benefit this year 2026, is only $986.35. Roughly 2.1 million Americans currently receive a benefit under their spouse’s earnings record. I wonder how many are being overpaid.

Seventh, do a thorough audit to determine if any illegal aliens are receiving any type of Social Security payments. Terminate their payments immediately. AND, cancel, delete, terminate, all Social Security numbers that Biden gave to his “newcomers.”

SENATOR CASSIDY WANTS TO SAVE SOCIAL SECURITY

Republican Senator Bill Cassidy of Louisiana has one big task he would like to check off his to-do list before his last day in office: Social Security reform. [That begs the question: why hasn’t he done anything these last 12 years?] Cassidy, a two-term senator, failed in May to win his Republican primary reelection bid against US Representative Julia Letlow and state Treasurer John Fleming. President Donald Trump endorsed Letlow, who won the primary. Now Cassidy, whose term officially ends on January 3, 2027, has vowed to get as much done as he can in his final days in office, including addressing Social Security, sometimes called the third rail of politics because of the potential consequences for leaders in office who enact changes to the program from which 71 million Americans (Are they all Americans?) receive monthly payments.

“The longer you wait, the harder it is to fix, the more painful to fix,” Cassidy told CNBC.com on June 10th in an interview outside the Capitol building. “We need to do something now.”

Social Security reform will have to be bipartisan, since legislation on the program requires 60 votes in the Senate. Some Democrats have proposed raising taxes on the “wealthy” to help shore up Social Security’s finances (that would produce very little extra taxes) while also increasing benefits. Meanwhile, Republicans largely oppose tax hikes, which leaves raising the retirement age and/or cutting monthly payments and/or enacting Cassidy’s “big idea” as the only apparent options.

CASSIDY’S “BIG IDEA”

Cassidy has come up with what he calls a “big idea” plan that mostly sidesteps the dilemma of raising taxes or cutting benefits. Instead, the proposal calls for investing $1.5 trillion in an investment fund separate from Social Security’s trust funds over five years. Over 65 to 70 years, that money that would be invested in the stock market would grow to 60% to 65% of Social Security’s unfunded accrued liability, Cassidy said. Senator Tim Kaine (D-VA) has joined him in promoting this “big idea.”

While the $1.5 trillion would be borrowed, it wouldn’t increase the nation’s debt, since it would be held in an escrow account and would therefore stay in the government’s possession, according to Cassidy. The plan is modeled after changes enacted to the federal Railroad Retirement system under President George W. Bush that allowed the pension funds to be invested in private securities. Investing on behalf of the railroad program improved its solvency, Cassidy said, and could be a model for Social Security. Notably, the change was enacted on a bipartisan basis, Cassidy said.

Cassidy said crafting the proposal has included an analysis of what would have happened during past market blips and found there would be an investment premium representing a higher return than the cost of borrowing. “All risk is borne by the fund, people would get their promised benefits,” Cassidy said.

It remains to be seen whether the proposal will win broader political support on Capitol Hill or from the White House. To be sure, the idea may also be a tough sell with some Democrats, who have proposals in both the House and Senate to extend the program’s solvency through a combination of raising taxes and increasing benefits. Increasing benefits? Say what?

Senators who have been working on Social Security proposals for a long time should have the opportunity to present them, Durbin said during a June 10th Senate floor speech. “But to do that, we have to do something we haven’t done in a long time,” Durbin said. “Get ready. Buckle your seatbelts. I’m talking about legislating, actually bringing a measure to the floor and opening it to amendment.”

In June, Sen. Elizabeth Warren (D-MA) warned that raising the retirement age by two years could effectively cut lifetime benefits by 17% to 35%, arguing the move would disproportionately hurt lower-income workers and those in physically demanding jobs.

Since Americans are living longer, yours truly believes raising the minimum age for receiving retirement benefits to 70 for anyone born in for after 1970 would be one of the ways to save the program.^

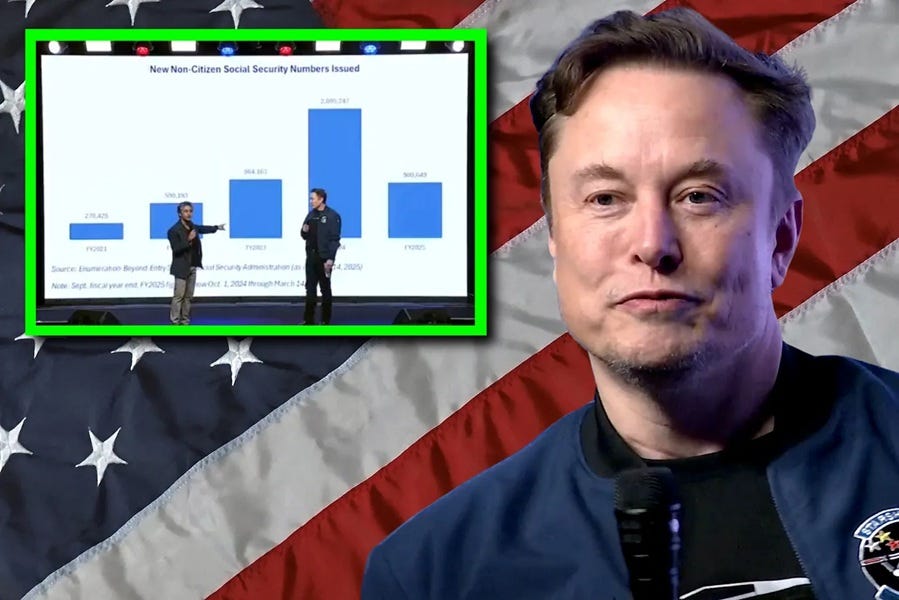

Elon Musk Reveals Shocking Surge in Social Security Numbers for Illegals

A speech Elon gave in Wisconsin over the weekend was absolutely mind boggling. If you don’t have time to watch the entire speech, please fast forward to the 39-minute mark in this video where Elon and a DOGE staffer explai…

^Your truly had a part-time job waiting for me when I turned age 16 and became eligible to obtain a Social Security number. Ten days after I graduated from high school I had my first full-time job. Thereafter, I worked full-time & overtime until I was three months shy of my 72nd birthday.

The author, Diane L. Gruber, is a First Amendment advocate who writes for Substack. She calls her Substack newsletter America First Re-Ignited. Follow me on X @DianeLGruber.

If you enjoyed this article, then please REPOST or SHARE with others; encourage them to follow AFNN. If you’d like to become a citizen contributor for AFNN, contact us at managingeditor@afnn.us. Help keep us ad-free by donating here.

Substack: American Free News Network Substack

Truth Social: @AFNN_USA

Facebook: https://m.facebook.com/afnnusa

Telegram: https://t.me/joinchat/2_-GAzcXmIRjODNh

Twitter: https://twitter.com/AfnnUsa

GETTR: https://gettr.com/user/AFNN_USA

CloutHub: @AFNN_USA

Patriot.Online: @AFNN